Business Loan Form Template - Facilitating the Applicant's Commercial Credit Assessment

Commercial credit underwriting often stalls during the initial intake phase, frustrating applicants and loan officers alike. When seeking capital through traditional banks or credit unions, gathering required disclosures remains a primary bottleneck. The Applicant power tool resolves this friction, granting underwriters immediate, structured access to verified borrower profiles.

While compliance stipulations require a meticulous assessment of debt-to-income ratios and collateral, the documentation process should not impede momentum. By automating the collection of complex files-such as balance sheets, tax returns, and cash flow statements-Applicant safeguards accuracy. Below, we explore how integrating our Business Loan Form Template optimizes this critical credit assessment pipeline.

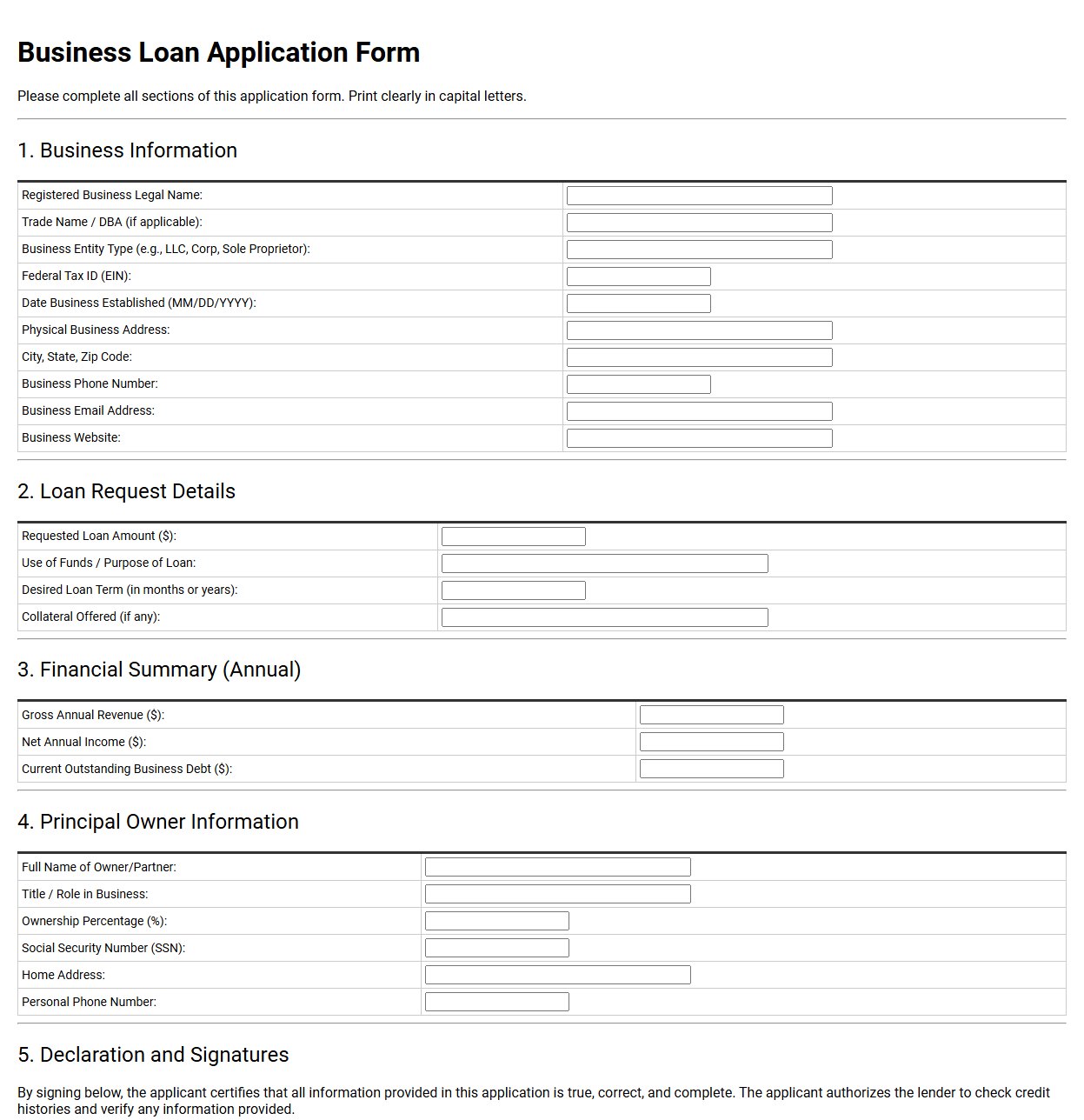

Business Loan Application Form Template

💾 Business Loan Application Form Template .pdf

A business loan application form template structures critical financial and organizational data for lenders. It captures company details, revenue history, requested funding amounts, and collateral specifications. This document helps financial institutions assess creditworthiness and risk. It streamlines the underwriting process, ensuring applicants submit necessary records to secure vital commercial financing.

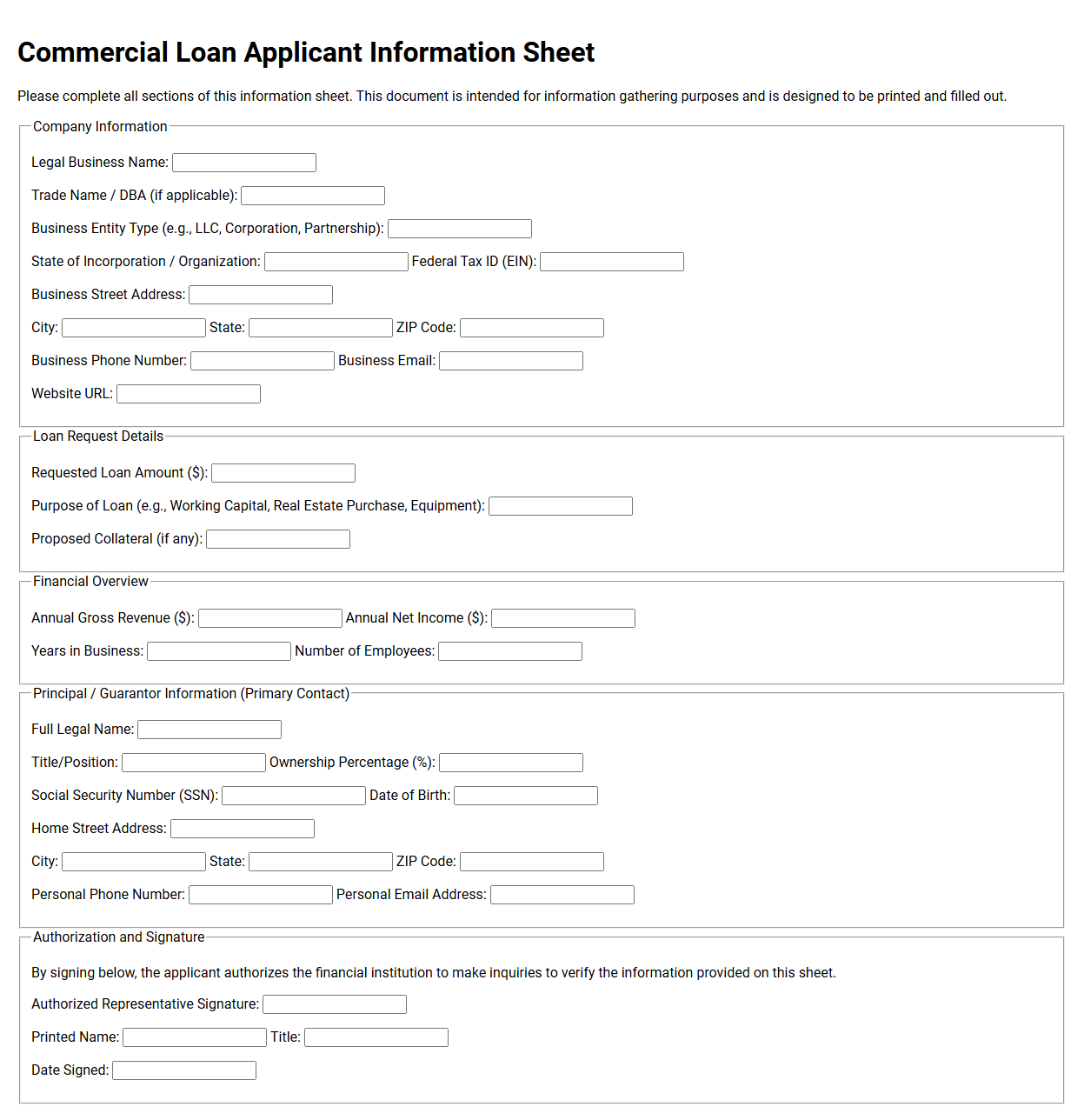

Commercial Loan Applicant Information Sheet

💾 Commercial Loan Applicant Information Sheet .pdf

A commercial loan applicant information sheet is a standard document that gathers crucial financial and organizational details. It collects business names, tax identification numbers, ownership structures, and contact information. Lenders utilize this data to assess creditworthiness, verify legal identities, and initiate the formal underwriting process for business financing.

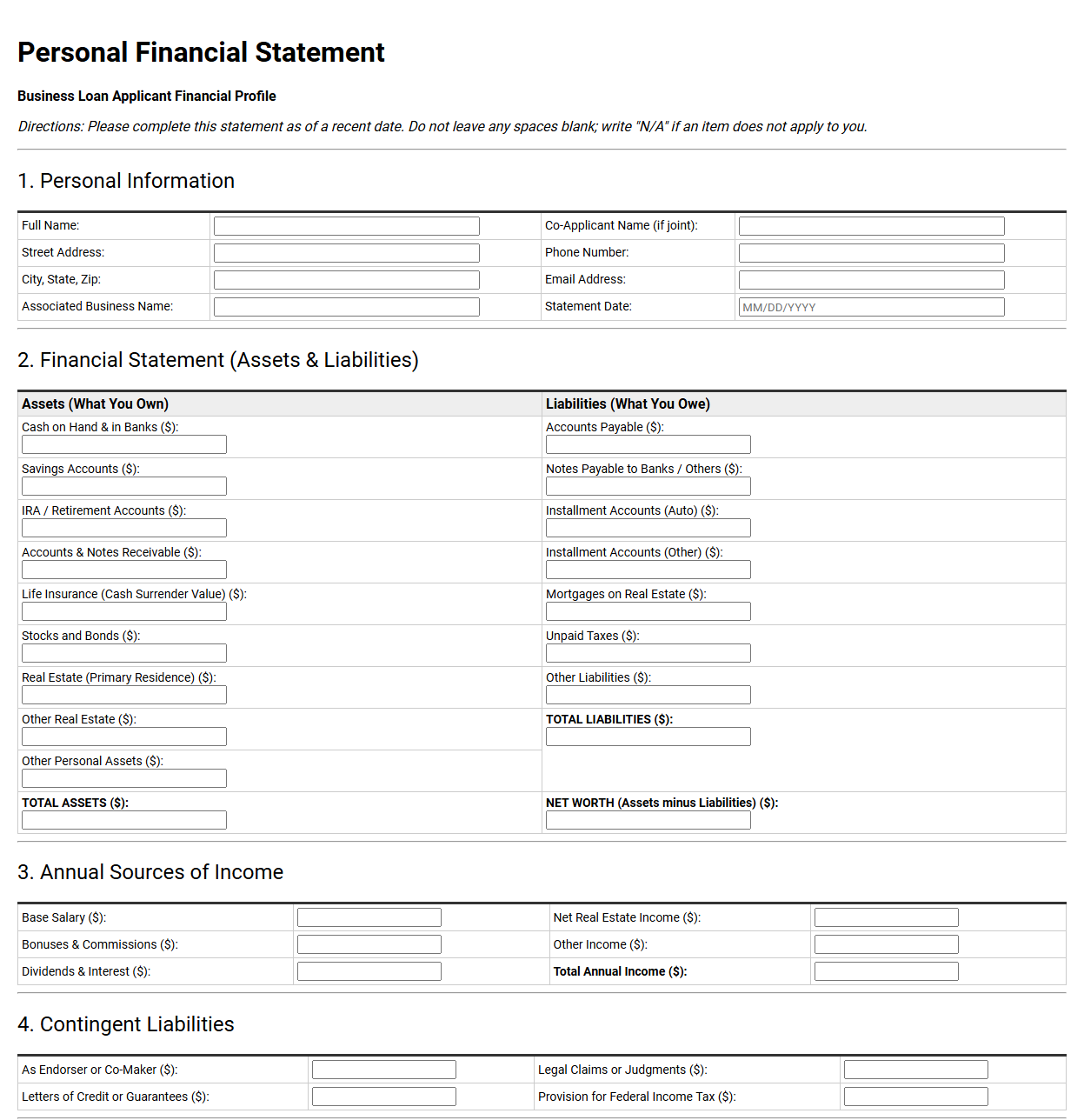

Personal Financial Statement for Business Loan Applicants

💾 Personal Financial Statement for Business Loan Applicants .pdf

A personal financial statement details a business loan applicant's individual assets, liabilities, and net worth. Lenders use this document to assess the borrower's financial health and ability to personally guarantee the debt. It typically outlines cash, investments, real estate holdings, outstanding credit card balances, and personal loans.

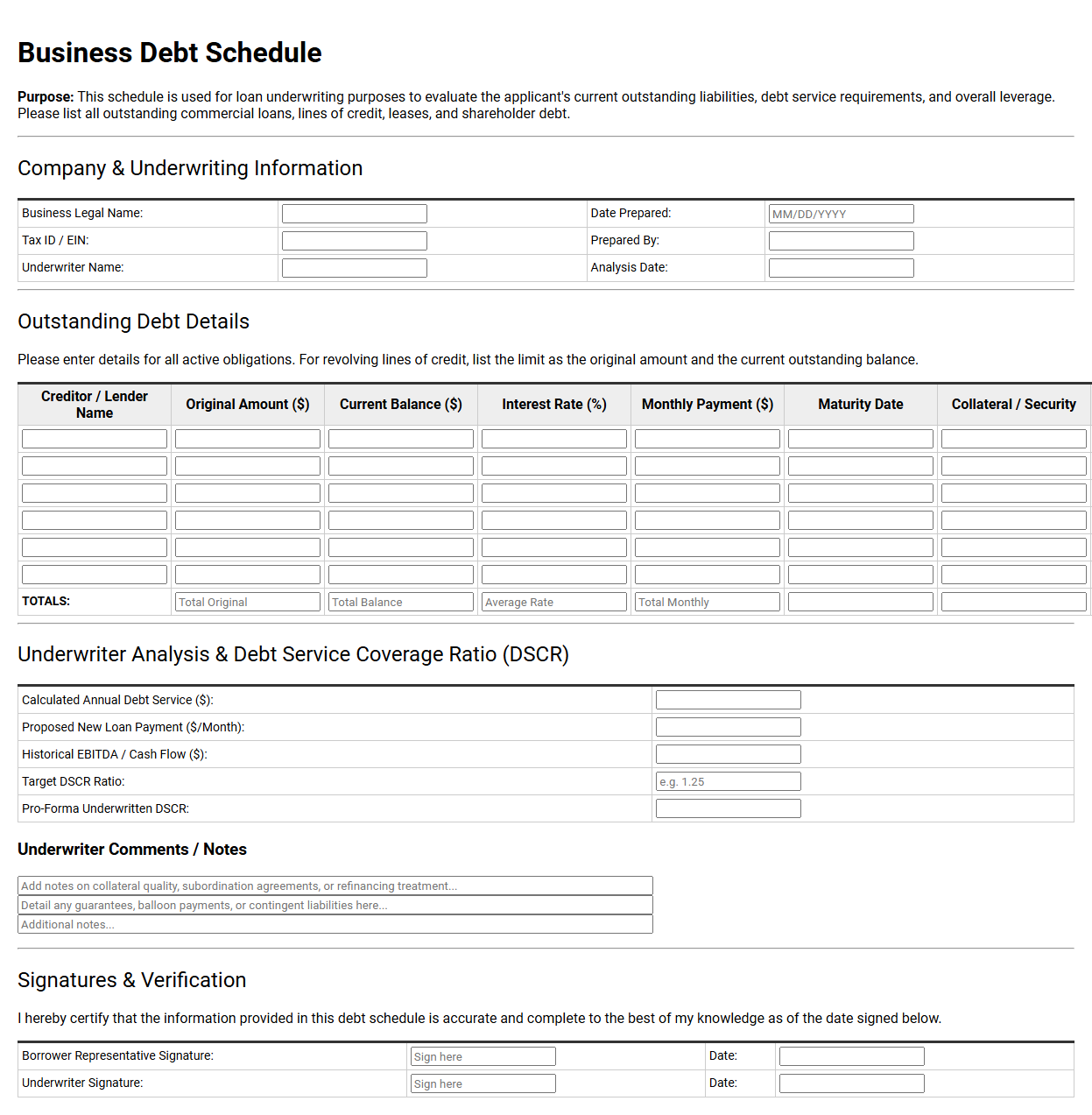

Business Debt Schedule Template for Loan Underwriting

💾 Business Debt Schedule Template for Loan Underwriting .pdf

A business debt schedule template is a structured financial document used during loan underwriting to inventory a company's outstanding liabilities. It details current balances, interest rates, monthly payments, and maturity dates. Lenders analyze this data to evaluate cash flow viability and calculate key debt service coverage ratios for final approval.

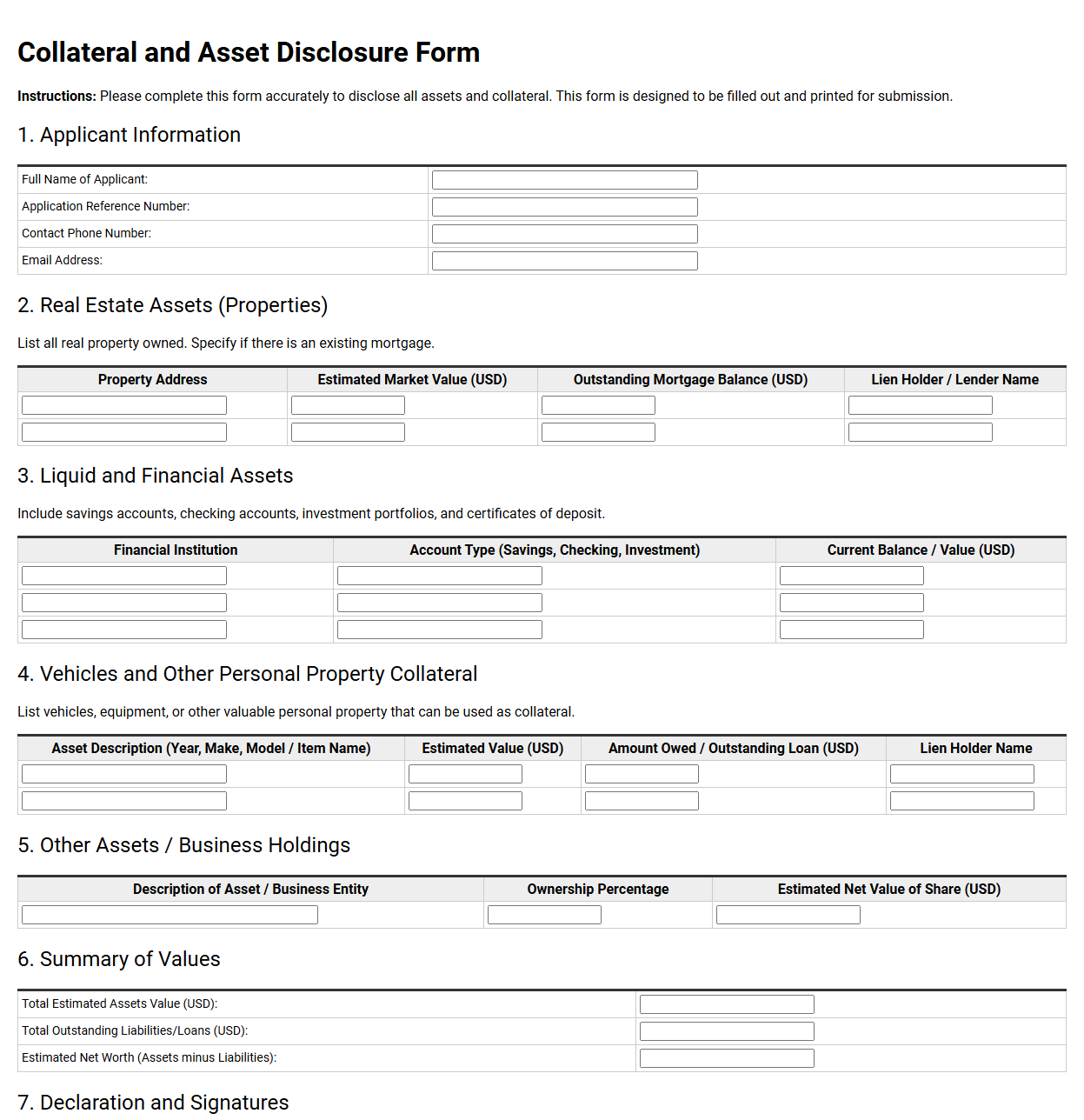

Collateral and Asset Disclosure Form for Applicants

💾 Collateral and Asset Disclosure Form for Applicants .pdf

This document requires applicants to declare their financial holdings, real estate, and valuable personal property. Lenders utilize this detailed record to evaluate net worth and establish security for credit. Accurate completion guarantees a transparent assessment of financial strength, helping institutions determine loan eligibility and structure appropriate borrowing terms safely.

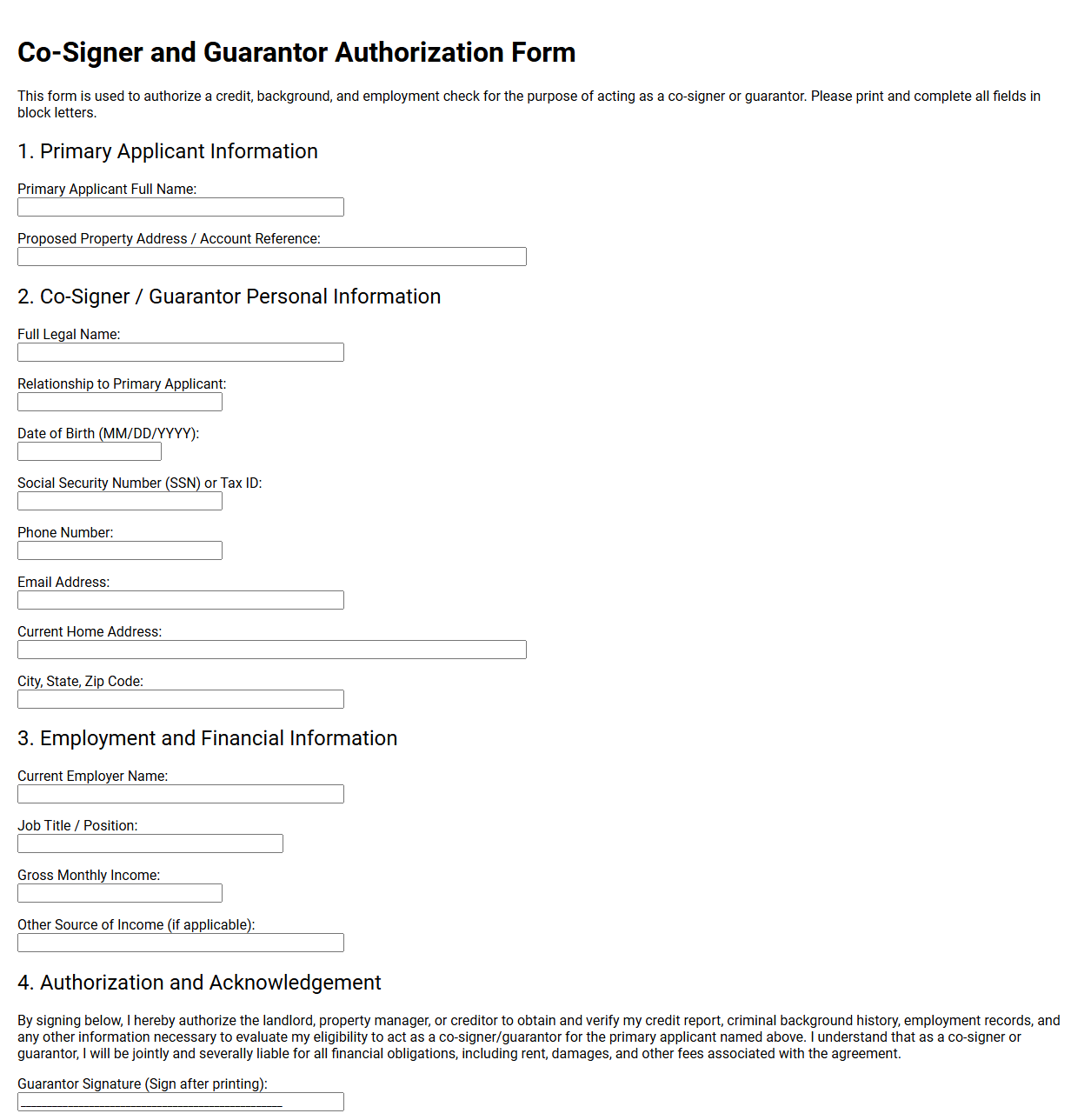

Co-Signer and Guarantor Authorization Form

💾 Co-Signer and Guarantor Authorization Form .pdf

A Co-Signer and Guarantor Authorization Form is a legal document permitting creditors or landlords to conduct background and credit checks on a secondary financial party. Through this instrument, the underwriting guarantor formally consents to assume full financial liability for the contract if the primary applicant fails to meet their payment obligations.

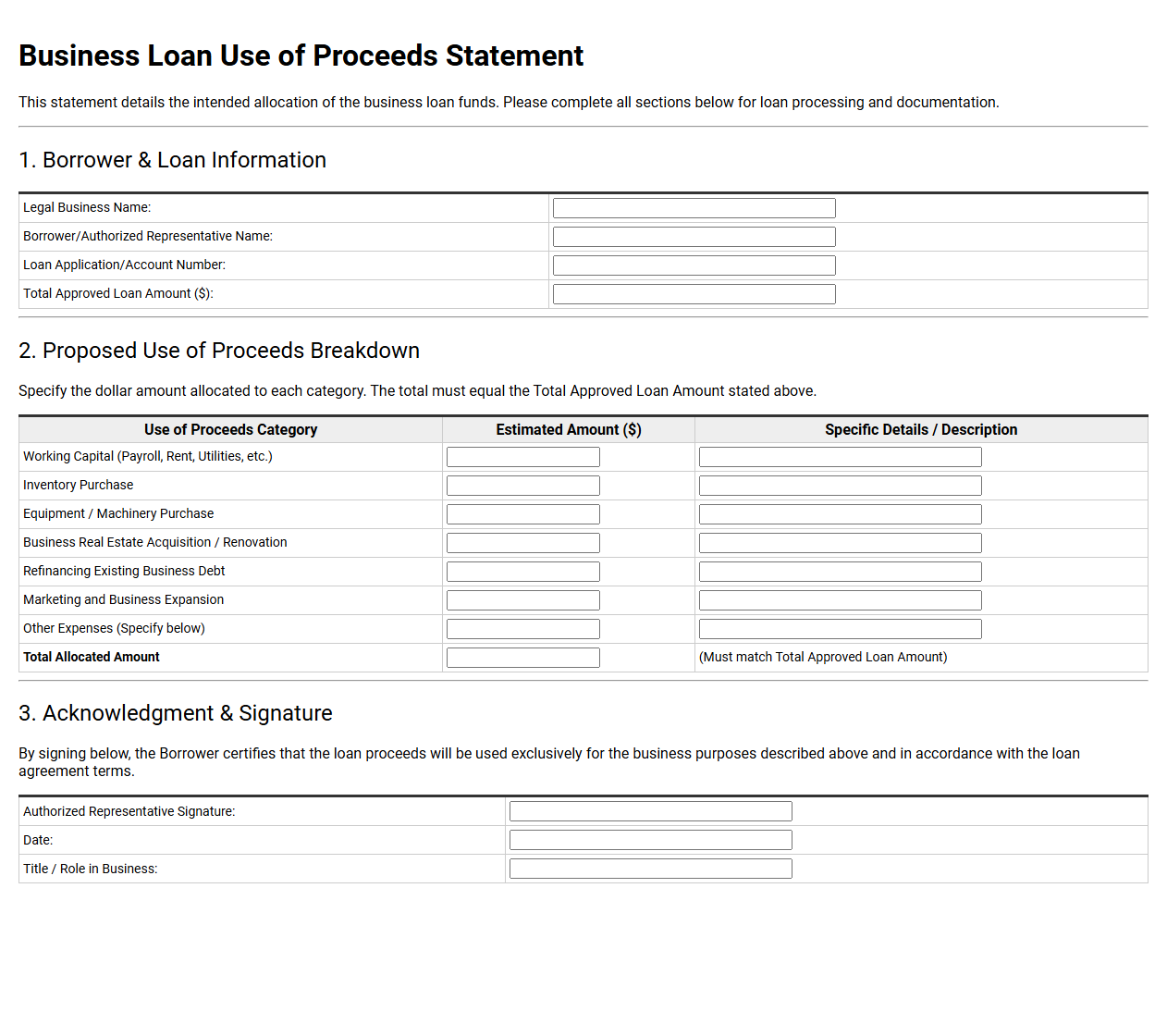

Business Loan Use of Proceeds Statement

💾 Business Loan Use of Proceeds Statement .pdf

A Business Loan Use of Proceeds Statement is a formal document detailing how a borrower plans to allocate acquired capital. Lenders require this breakdown to assess risk and ensure funds support growth, such as purchasing inventory, hiring staff, or acquiring real estate, securing alignment with the loan terms.

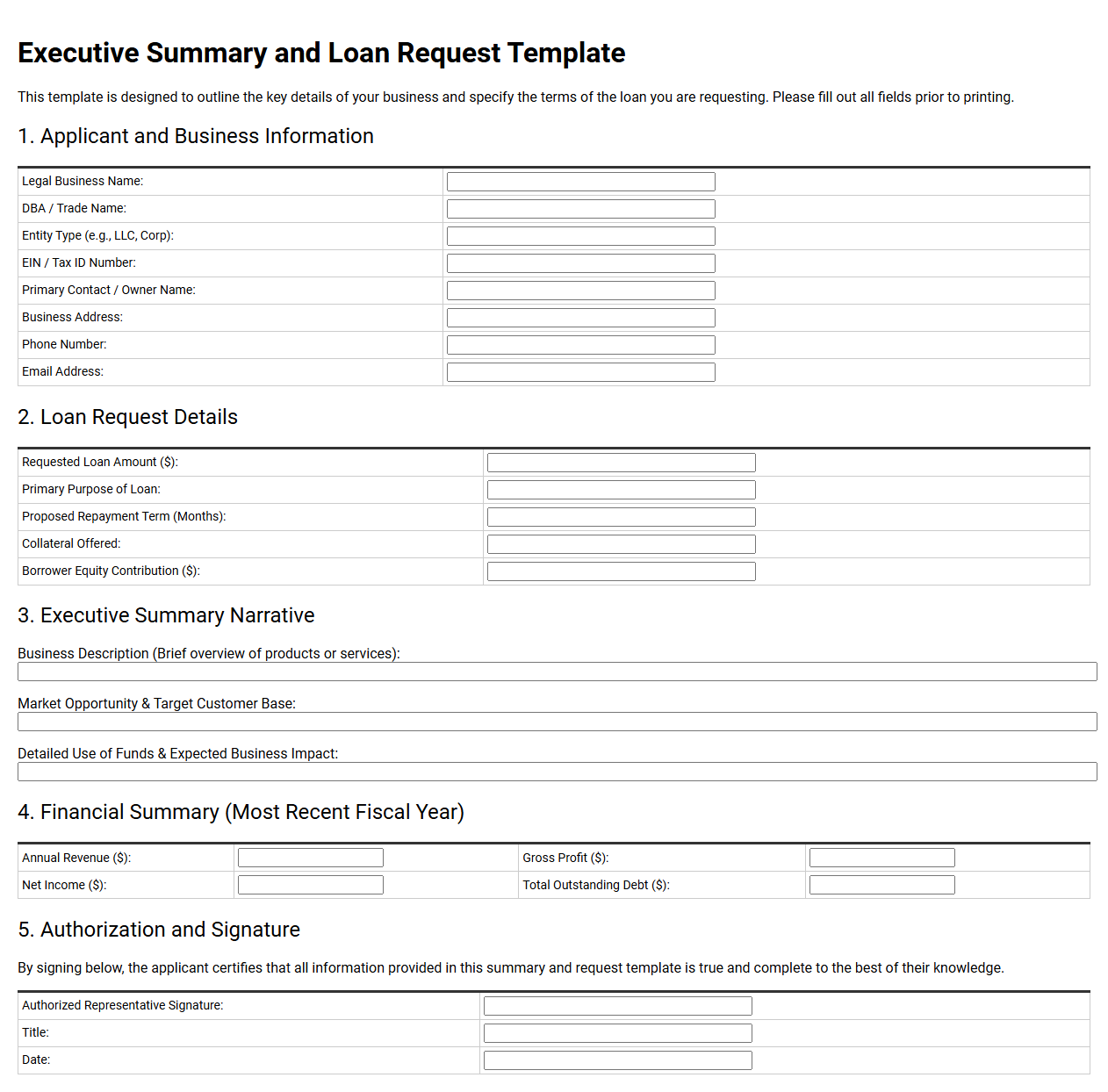

Executive Summary and Loan Request Template

💾 Executive Summary and Loan Request Template .pdf

A standard executive summary and loan request template outlines a business's financial health, funding needs, and repayment strategies. It provides lenders with a clear overview of the company's operations, market position, and historical growth. This structured document successfully guides applicants in presenting a compelling case to secure critical business capital.

Applicant Credit History Authorization Form

💾 Applicant Credit History Authorization Form .pdf

An Applicant Credit History Authorization Form is a formal document granting landlords or employers permission to acquire a consumer credit report. This record verifies financial responsibility, payment history, and outstanding debts. By signing, applicants consent to background checks, facilitating informed leasing or hiring decisions based on demonstrated fiscal reliability.

Business Cash Flow Projection Template for Lenders

💾 Business Cash Flow Projection Template for Lenders .pdf

A business cash flow projection template for lenders illustrates a company's financial viability. This structured document forecasts incoming revenues and outgoing expenses over a specific period. It helps financial institutions evaluate your capacity to repay debt, demonstrating fiscal responsibility and highlighting future liquidity trends required for securing commercial loans.

Business Loan Application Checklist Document

💾 Business Loan Application Checklist Document .pdf

A business loan application checklist is a vital document outlining the necessary paperwork required by lenders. It typically lists financial statements, tax returns, business plans, and legal documents. This guide helps entrepreneurs organize their files, ensuring a smooth evaluation process and accelerating the timeline for securing capital.

Profit and Loss Statement Template for Applicants

💾 Profit and Loss Statement Template for Applicants .pdf

A profit and loss statement template helps applicants present their financial standing. This document details revenues, costs, and business expenses over a specific period. Landlords or lenders use it to assess financial stability, verifying if the business generates sufficient net income to meet all future lease or loan commitments reliably.

Applicant Business Loan FAQ

What are the primary eligibility criteria for a business loan applicant?

Lenders evaluate your credit score, annual revenue, and operational history, typically requiring at least two years in business. They also assess your debt-to-income ratio and business plan to ensure you possess the cash flow and financial stability required to repay the borrowed capital.

What is the difference between secured and unsecured business loans?

Secured loans require physical collateral, like property or equipment, which lenders can seize upon default. Unsecured loans require no collateral but carry higher interest rates and stricter credit requirements, as the lender assumes higher risk without asset backing.

How do lenders determine interest rates for applicant business loans?

Lenders calculate interest rates using market benchmarks, your business's creditworthiness, industry risk, and loan terms. Stronger financial health, excellent credit history, and valuable collateral typically secure lower rates, while riskier ventures face higher borrowing costs.

What purposes can an applicant use business loan funds for?

Business loans fund essential operations like purchasing inventory, acquiring equipment, refinancing existing debt, or managing payroll. Lenders evaluate how these funds will generate revenue, ensuring the capital directly supports business growth and sustained financial health.

Why is the Debt-Service Coverage Ratio critical for loan applicants?

The Debt-Service Coverage Ratio, or DSCR, measures your company's cash flow against its debt obligations. Lenders analyze this ratio to verify that your business generates sufficient operating income to comfortably cover both existing debts and new loan repayments.

Disclaimer:

The documents and templates provided on this page are for informational and illustrative purposes only. They do not constitute professional, legal, or financial advice, and should not be relied upon as such. Because individual circumstances and regulatory requirements vary, these materials may not be suitable for your specific needs. We recommend consulting with a qualified professional before adapting or using any of these examples for official or commercial purposes.